The oil and gas sector, one of the major emitters of planet-warming gases, will need a rapid and substantial overhaul for the world to avoid even worse extreme weather events fueled by human-caused climate change, according to The Oil and Gas Industry in Net Zero Transitions, report by International Energy Agency (IEA), released Thursday.

The special report was released before the UN climate summit, or COP28, which begins in Dubai next week, and sets out what the industry must do to align itself with the Paris Agreement.

Oil and gas companies, and other people and organizations connected to fossil fuels, often attend the meeting, drawing criticism from environmentalists and climate experts. Last year’s climate conference in Egypt saw 400 people connected with fossil fuel industries attending the event, according to an analysis by The Associated Press. The upcoming meeting has also come under fire for appointing the chief of the Abu Dhabi National Oil Company as the talks’ president. But others say the sector needs to be at the table to discuss how to transition to cleaner energy.

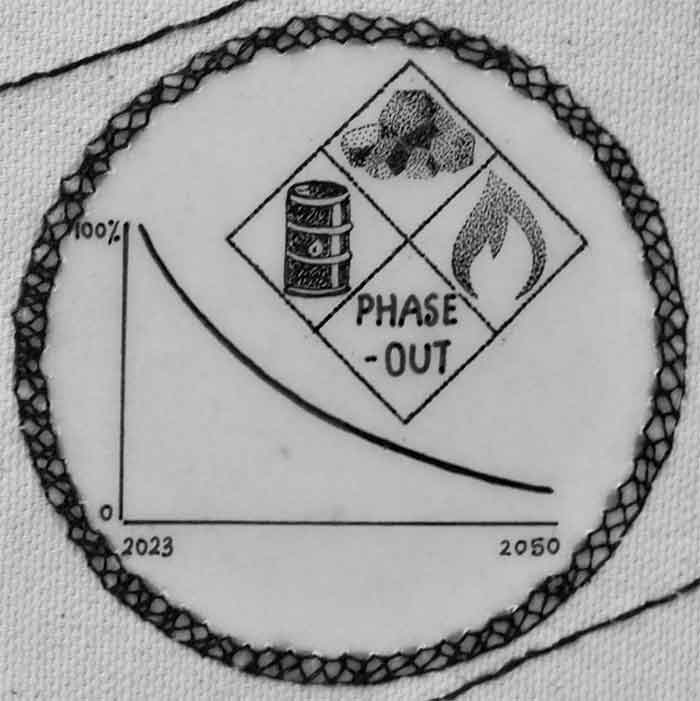

The current investment of $800 billion a year in the oil and gas sector will need to be cut in half and greenhouse emissions, which result from the burning of fossil fuels like oil, will need to fall by 60% to give the world a fighting chance to meet its climate goals, the IEA said. Greenhouse gases go up into the atmosphere and heat the planet, leading to several impacts, including extreme weather events.

Oil and gas companies can find alternative revenue from the clean energy economy, including hydrogen and hydrogen-based fuels and carbon capture technologies, the report said. Both clean hydrogen — made from renewable electricity — and carbon capture — which takes carbon dioxide out of the atmosphere — are currently untested at scale.

The global oil and gas industry encompasses a large and diverse range of players: from small, specialized operators to huge national oil companies. These producers face pivotal choices about their role in the global energy system amid a worsening climate crisis fuelled in large part by their core products.

This report explores what oil and gas companies can do to accelerate net zero transitions and what this might mean for an industry which currently provides more than half of global energy supply and employs nearly 12 million workers worldwide.

The Oil and Gas Industry in Net Zero Transitions report analyses the implications and opportunities for the industry that would arise from stronger international efforts to reach energy and climate targets.

The report also examines how transitions increase the likelihood of boom and bust cycles for oil and gas producer economies. It highlights strategies for producer economies that could complement broader reforms to build macroeconomic stability and the role of international partners to support this process.

The report sets out a fair and feasible way forward in which oil and gas companies and producer economies take a real stake in the clean energy economy while helping the world avoid the most severe impacts of climate change.

“The oil and gas industry is facing a moment of truth at COP28 in Dubai,” said Fatih Birol, executive director of the IEA in a press statement on the report’s release. “Oil and gas producers need to make profound decisions about their future place in the global energy sector.”

“The industry needs to commit to genuinely helping the world meet its energy needs and climate goals – which means letting go of the illusion that implausibly large amounts of carbon capture are the solution,” Dr Birol said.

“This special report shows a fair and feasible way forward in which oil and gas companies take a real stake in the clean energy economy while helping the world avoid the most severe impacts of climate change.”

If acted upon, there are opportunities for the oil and gas sector to invest in technology for clean energy transitions. Still, producers would have to put 50% of their capital towards clean energy projects by 2030.

“The fossil fuel sector must make tough decisions now, and their choices will have consequences for decades to come,” Dr Birol added.

“Clean energy progress will continue with or without oil and gas producers. However, the journey to net zero emissions will be more costly and harder to navigate if the sector is not on board.”

The energy sector is responsible for over two-thirds of all human activity-related greenhouse gas emissions, and oil and gas is responsible for about half of those, according to the IEA. Oil and gas companies are also responsible for over 60% of methane emissions — a gas that traps about 87 times more heat than carbon dioxide on a 20-year timescale.

The report looked at climate promises made by countries as well as a scenario where the world had reached net zero emissions by 2050. It found that if countries deliver on all climate pledges, demand for oil and gas will be 45% lower than today’s level by 2050. If the world reaches net zero by then, demand would be down 75%, it said.

Earlier this year, another IEA report found that the world’s oil, gas and coal demand will likely peak by the end of this decade.

The report says the industry’s emissions need to drop by 60% by 2030 to keep global warming to an increase of just 1.5C “within reach” and would have to reduce emissions by 75% to reach the 2050 net-zero goal.

The IEA report said:

- Structural changes in the energy sector are now moving fast enough to deliver a peak in oil and gas demand by the end of this decade under today’s policy settings. After the peak, demand is not currently set to decline quickly enough to align with the Paris Agreement and the 1.5 °C goal. But if governments deliver in full on their national energy and climate pledges, then oil and gas demand would be 45% below today’s level by 2050 and the temperature rise could be limited to 1.7 °C. If governments successfully pursue a 1.5 °C trajectory, and emissions from the global energy sector reach net zero by mid-century, oil and gas use would fall by 75% to 2050.

- Since 2018, the annual revenues generated by the oil and gas industry have averaged close to USD 3.5 trillion. Around half of this went to governments, while 40% went back into investment and 10% was returned to shareholders or used to pay down debt. The implications of net zero transitions are far from uniform: the industry encompasses a wide range of players, from small, specialized operators to huge national oil companies (NOCs). While attention often focuses on the role of the majors, which are seven large, international players, they hold less than 13% of global oil and gas production and reserves. NOCs account for more than half of global production and close to 60% of the world’s oil and gas reserves.

- Oil and gas producers account for only 1% of total clean energy investment globally. More than 60% of this comes from just four companies, out of thousands of producers of oil and gas around the world today. For the moment the oil and gas industry as a whole is a marginal force in the world’s transition to a clean energy system.

- Most oil and gas companies are watching energy transitions from the sidelines. While there is no single blueprint for change, there is one element that can and should be in all company transition strategies: reducing emissions from the industry’s own operations. As things stand, less than half of current global oil and gas output is produced by companies that have targets to reduce these emissions. A far broader coalition – with much more ambitious targets – is needed to achieve meaningful reductions across the oil and gas industry. The production, transport and processing of oil and gas results in just under 15% of global energy-related greenhouse gas emissions. This is a huge amount, equivalent to all energy-related greenhouse gas emissions from the United States.

- To align with a 1.5 °C scenario, these emissions need to be cut by more than 60% by 2030 from today’s levels and the emissions intensity of global oil and gas operations must near zero by the early 2040s. These are appropriate benchmarks for industry-wide action on emissions, regardless of the future scenario. The emissions intensity of the worst performers is currently five- to ten-times higher than the best. Methane accounts for half of the total emissions from oil and gas operations. Tackling methane leaks is a top priority and can be done very cost-effectively – but it is not the only priority.

- The first-order task is to slash emissions from company operations. The volatility of fossil fuel prices means that revenues could fluctuate from year to year – but the bottom line is that oil and gas becomes a less profitable and a riskier business as net zero transitions accelerate. Prices and output are generally lower and the risk of stranded assets is higher, especially in the midstream sector that includes refineries and facilities for liquefied natural gas. If expectations are that demand and prices follow a scenario based on today’s policy settings, that would value today’s private oil and gas companies at around USD 6 trillion. If all national energy and climate goals are reached, this value is lower by 25%, and by 60% if the world gets on track to limit global warming to 1.5 °C.

- Oil and gas projects currently produce slightly higher returns on investment, but those returns are less stable. IEA estimates that the return on capital employed in the oil and gas industry averaged around 6-9% between 2010 and 2022, whereas it was 6% for clean energy projects. Oil and gas returns varied greatly over time compared with more consistent returns for clean energy projects.

- Transitions will hurt the bottom line for companies focused on oil and gas. Continued investment in oil and gas supply is needed in all scenarios, but the USD 800 billion it currently invests each year is double what is required in 2030 to meet declining demand in a 1.5 °C scenario. Investment in existing and some new fields is necessary in a world that achieves national energy and climate pledges, although there is no need in aggregate for new exploration. In a scenario that hits global net zero emissions by 2050, declines in demand are sufficiently steep that no new long lead-time conventional oil and gas projects are required. Some existing production would even need to be shut in. In 2040, more than 7 million barrels per day of oil production is pushed out of operation before the end of its technical lifetime in a 1.5 °C scenario.

- In net zero transitions, new project developments face major commercial risks and could also lock in emissions that push the world over the 1.5 °C threshold. Producers need to explain how any new resource developments are viable within a global pathway to net zero emissions by 2050 and be transparent about how they plan to avoid pushing this goal out of reach.

- Oil and gas investment is needed in all scenarios, but the demand trajectory in a 1.5 °C world leaves no room for new fields. Many producers say they will be the ones to keep producing throughout transitions and beyond. They cannot all be right. Oil and gas production is vastly reduced in net zero transitions but does not disappear. Even in a 1.5 °Cscenario, some 24 million barrels per day of oil is produced in 2050 (three-quarters is used in sectors where the oil is not combusted, notably in petrochemicals), as well as some 920 billion cubic metres of natural gas, roughly half of which is used for hydrogen production.

- The distribution of future supply among producers will depend on the weight assigned to lowering costs, ensuring diversity of supply, reducing emissions, and fostering economic development. Market forces naturally favour the lowest-cost production, but that leads to a high concentration in supply among today’s major resource holders, notably in the Middle East. Prioritizing the least emissions-intensive sources drives progress towards climate goals, but this often favors low-cost producers, so supply still becomes more concentrated. It is much better for transitions if all producers take targeted action to reduce their emissions. If production from low-income producers is favored, these projects may not ultimately be very profitable in a well-supplied market. And if countries prefer domestically produced oil and gas as a way to buttress energy security, they reduce reliance on others but risk finding themselves with relatively high-cost projects in a low-price world.

- Not all producers can be the last ones standing. Some 30% of the energy consumed in a net zero energy system in 2050 comes from low-emissions fuels and technologies that could benefit from the skills and resources of the oil and gas industry. These include hydrogen and hydrogen-based fuels; carbon capture, utilization and storage (CCUS); offshore wind; liquid biofuels; biomethane; and geothermal energy. Oil and gas companies are already partners in a large share of planned hydrogen projects that use CCUS and electrolysis. The oil and gas industry is involved in 90% of CCUS capacity in operation around the world. CCUS and direct air capture are important technologies for achieving net zero emissions, especially to tackle or offset emissions in hard-to-abate sectors. For the moment, only around 2% of offshore wind capacity in operation was developed by oil and gas companies. Plans are expanding, however, and the technology frontier for offshore wind – including floating turbines in deeper waters – moves this sector closer to areas of oil and gas company strength. In addition, industry skills and infrastructure, including existing retail networks and refineries, give the industry advantages in areas like electric vehicle charging and plastic recycling.

- The oil and gas industry is well placed to scale up some crucial technologies for net zero transitions…

- Companies that have announced a target to diversify their activities into clean energy account for just under one-fifth of current oil and gas production. The oil and gas industry invested around USD 20 billion in clean energy in 2022, some 2.5% of its total capital spending. In this report, we offer a new framework for assessing the strategies of oil and gas companies and the extent to which they are making a meaningful contribution to transitions. For producers that choose to diversify and are looking to align with the aims of the Paris Agreement, our bottom-up analysis of cash flows in a 1.5 °C scenario suggests that a reasonable ambition is for 50% of capital expenditures to go towards clean energy projects by 2030, on top of the investment needed to reduce scope 1 and 2 emissions.

- Not all oil and gas companies have to diversify into clean energy, but the alternative is to wind down traditional operations over time. Some companies may take the view that their specialisation is in oil and natural gas and so decide that – rather than risking money on unfamiliar business areas – others are better placed to allocate this capital. But aligning their strategies with net zero transitions would then require them to scale back oil and gas activities while investing in scope 1 and 2 emissions reductions. …but this requires a step-change in the industry’s allocation of investment.

- A productive debate about the oil and gas industry in transitions needs to avoid two common misconceptions. The first is that transitions can only be led by changes in demand. “When the energy world changes, so will we” is not an adequate response to the immense challenges at hand. An imbalanced focus on reducing supply is equally unproductive, as it comes with a heightened risk of price spikes and market volatility. In practice, no one committed to change should wait for someone else to move first. Successful, orderly transitions are collaborative ones, in which suppliers work with consumers and governments to expand new markets for low-emissions products and services.

- The second is excessive expectations and reliance on CCUS. Carbon capture, utilization and storage is an essential technology for achieving net zero emissions in certain sectors and circumstances, but it is not a way to retain the status quo. If oil and natural gas consumption were to evolve as projected under today’s policy settings, this would require an inconceivable 32 billion tonnes of carbon captured for utilization or storage by 2050, including 23 billion tonnes via direct air capture to limit the temperature rise to 1.5 °C. The necessary carbon capture technologies would require 26 000 terawatt hours of electricity generation to operate in 2050, which is more than global electricity demand in 2022. And it would require over USD 3.5 trillion in annual investments all the way from today through to mid-century, which is an amount equal to the entire industry’s annual average revenue in recent years.

- Economies that are heavily reliant on oil and gas revenues face some stark choices and pressures in energy transitions. These choices are not new, but the prospect of falling oil and gas demand adds a timeline and a deadline to the process of economic diversification. Transitions create powerful incentives to accelerate the pace of change while also draining a source of revenue that could finance it. Compared with the annual average between 2010 and 2022, per capita net income from oil and natural gas among producer economies is 60% lower in 2030 in a 1.5 °C scenario. New producers entering the market face additional challenges, as they may overestimate the bounty that might lie ahead and underestimate the hazards. Many producers are also heavily exposed to risks from a changing climate, which stand to further disrupt the security of energy supply.

- The challenges are formidable, but there are workable net zero energy strategies available to producer economies and national oil companies. Today’s producer economies retain energy advantages even as the world moves away from fossil fuels. In most cases, today’s major producers of low-cost hydrocarbons also have expertise and ample, underutilized renewable energy resources that could anchor positions in clean energy value chains and low-emissions industries. Reducing emissions from traditional supplies, including end‑use emissions; putting domestic energy systems on a cleaner footing by phasing out inefficient subsidies and boosting clean energy deployment; and developing low-emissions products and services offer a way forward.

- Producer economies face major uncertainties, but their energy advantages are not lost in transition. Our scenarios plot out how the transition could be achieved, but the baseline expectation should be for a volatile and bumpy ride. Declining markets are difficult to plan for, and the potential for disruption also comes from geopolitical tensions and increased incidences of extreme weather. Governments need to be vigilant for risks to the affordability and security of supply. The implications of any physical disruptions to supply are felt most strongly in emerging and developing economies in Asia, whose share of global crude oil imports rises from 40% today to 60% in 2050 in a scenario that meets national energy and climate goals. On the supply side, even as overall demand falls back, the Middle East plays an outsize role in global markets as a low-cost producer of both oil and gas.

- Dialogue across all parts of oil and gas value chains remains essential to deliver an orderly shift away from fossil fuels – and to ensure that today’s producers have a meaningful stake in the clean energy economy. The industry must change, but this dialogue also needs clear signals from consumers on the direction and speed of travel to guide investment decisions, to assign value to oil and gas with lower emissions intensities, to develop markets for low-emissions fuels, and to collaborate on technology innovation. Energy transitions can happen without the engagement of the oil and gas industry, but the journey to net zero will be more costly and difficult to navigate if they are not on board.

The report also said:

- Around 97 mb/d of oil and 4 150 bcm of natural gas were consumed globally in 2022. This resulted in just over 18 Gt CO2 emissions, around half of total energy-related CO2 emissions. Recent momentum in deploying clean energy technologies means that oil and gas demand peak before 2030 in the Stated Policies Scenario (STEPS), but the declines after these peaks are not steep enough to achieve the world’s climate goals.

- Net zero transitions require a huge acceleration in clean energy technology deployment and faster reductions in oil and gas use. In the Announced Pledges Scenario (APS), oil and gas demand decline by around 2% each year on average to 2050 (to 55 mb/d and 2 400 bcm) and in the Net Zero Emissions by 2050 (NZE) Scenario they fall by more than 5% each year on average to 2050 (to 24 mb/d and 920 bcm).

- Attention on the oil and gas industry often focuses on the large international oil and gas companies (the “majors”), but they own less than 13% of global oil and gas production and reserves. By comparison, national oil companies own more than half of production and close to 60% of reserves.

- Major challenges lie ahead for midstream infrastructure in net zero transitions. The refining sector reduces its output of traditional products like gasoline and diesel, and focuses more on petrochemical feedstocks and products like asphalt and bitumen. Global liquefied natural gas (LNG) trade sees strong near-term growth, but trade peaks in the APS before 2035 and the utilization of export terminals drops; in the NZE Scenario, demand for LNG can be met in aggregate by plants already in operation.

- In the APS and NZE Scenario, investment in existing oil and gas assets continues, but with very different outcomes for new project development. In the APS, new oil and gas projects are needed, although in aggregate there would be no need for further oil and gas exploration. In the NZE Scenario, falling demand means that no new long lead time conventional oil and gas projects are approved for development and, after 2030, a number of projects are closed before they reach the end of their technical lifetime.

- Many producers have set out why they think their resources should be preferred for development in net zero transitions. Some say that they have the lowest production costs or emission intensities; others claim that they are a better option for energy security; and some indicate that new oil and gas developments are needed to improve welfare. In the demand environment of the NZE Scenario, any new oil and gas resource developments would need to be matched by production reductions elsewhere to avoid oversupply and fossil fuel lock‑in.

- Both over- and underinvestment in fossil fuels carry risks for secure and affordable transitions. Sequencing the decline in oil and gas investment and the increase in clean energy investment is vital to avoid damaging price spikes or supply gluts. At present, risks appear to be weighted more towards overinvestment than the opposite.